Buying your first home in North Vancouver is one of the most significant financial decisions you will ever make. Done well, it sets you up for long term wealth building in one of Canada's most resilient real estate markets. Done without preparation, it can be an expensive and stressful experience that leaves you feeling like you missed something important.This guide covers everything a first time buyer needs to know about purchasing in North Vancouver in 2026 — the government programs available to you, the mistakes to avoid, the neighbourhoods worth considering, and what the buying process actually looks like from start to finish.

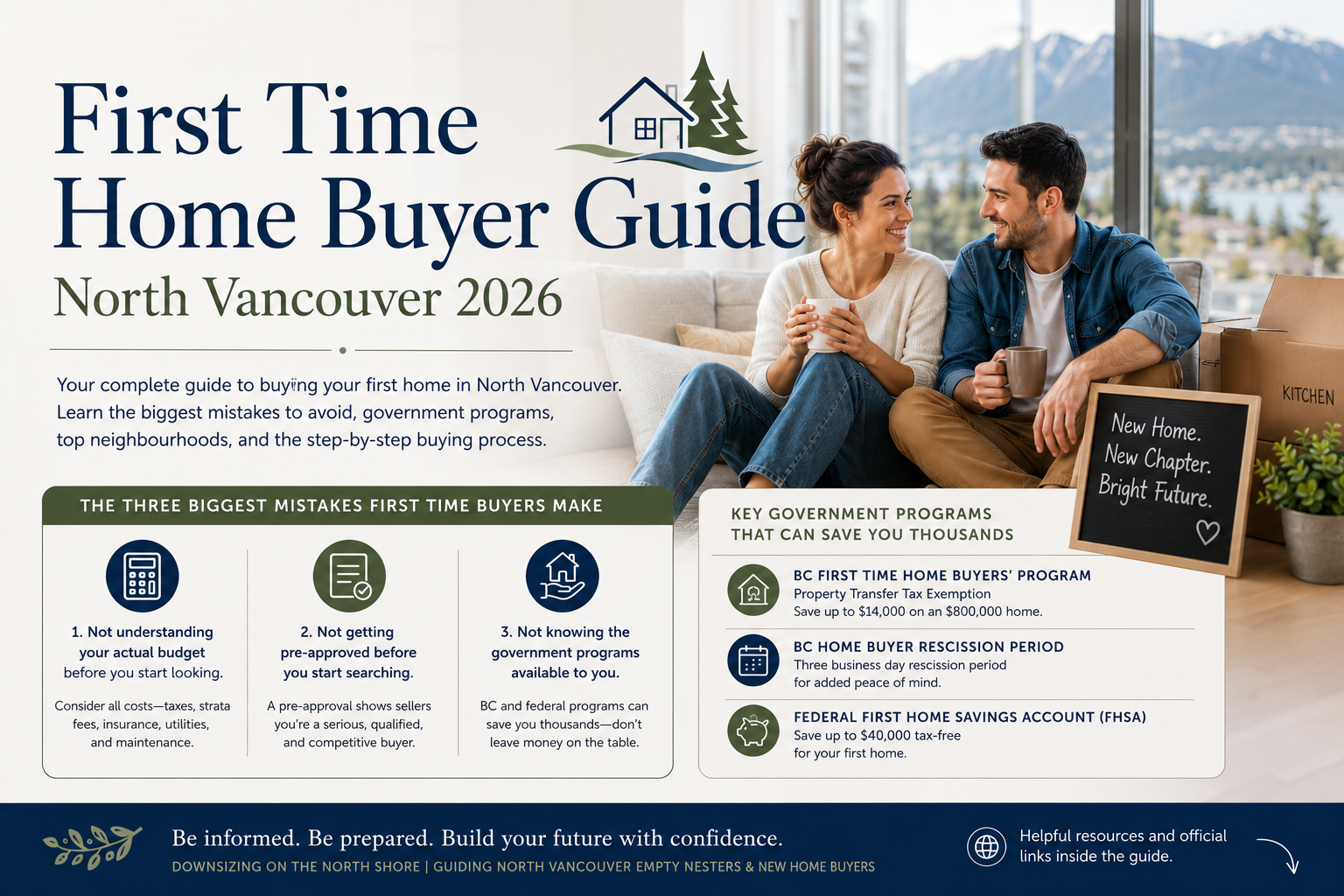

The Three Biggest Mistakes First Time Buyers Make

Before anything else, let's talk about what goes wrong — because avoiding these three mistakes will save you time, money, and frustration.Mistake 1: Not understanding your actual budget before you start looking.This is the most common and most costly mistake first time buyers make. Browsing listings before you have a clear picture of what you can afford sets you up for disappointment at best and a financially stretched purchase at worst. Your budget is not just your maximum mortgage approval — it's the full picture. And for most first time buyers, the full picture includes costs they haven't fully thought through yet.Beyond your down payment and mortgage payment, owning a home in North Vancouver comes with ongoing monthly and annual costs that add up quickly:Property taxes on a North Vancouver condo or townhome typically run $2,000 to $4,000 per year depending on assessed value and property type. Detached homes run higher.Strata fees for condos and townhomes vary significantly by building. Older buildings with more amenities can run $500 to $800 per month or more. Newer buildings with fewer amenities may be $300 to $500. Always review the strata financials and depreciation report before buying — underfunded strata reserves can lead to special assessments that cost owners thousands unexpectedly.Home insurance for a condo typically runs $100 to $200 per month. Detached home insurance is higher and varies by property age, size, and condition.Hydro and utilities in BC average $100 to $200 per month for a condo or townhome, higher for a detached home depending on size and heating type.Internet and cable — budget $100 to $200 per month depending on your provider and package.Maintenance and repairs — even in a strata property where the building exterior is covered, you are responsible for your own unit. Budget a minimum of $100 to $200 per month as a reserve for appliance repairs, plumbing issues, and general maintenance.Add all of this to your mortgage payment and you have a realistic picture of what homeownership actually costs month to month. Knowing this number before you start looking — not after you've made an offer — is what separates a confident buyer from a stressed one.Mistake 2: Not getting pre-approved before you start actively searching.A mortgage pre-approval is not the same as a pre-qualification. A pre-approval involves a full review of your income, employment, credit, and assets by a lender, and results in a written commitment for a specific loan amount at a specific rate. In a market where desirable properties still generate multiple offers, sellers look immediately at the strength of your financing. Without a pre-approval letter, you are not a competitive buyer. Get it done before you walk into a single open house.Mistake 3: Not knowing the government programs available to you as a first time buyer.First time buyers in BC have access to meaningful financial assistance that can reduce your upfront costs significantly. Most buyers either don't know these programs exist, don't understand how they work, or apply for them too late. We cover all of them below — read this section carefully before you do anything else.Government Programs Every First Time Buyer in BC Should Know

These are real programs with real financial impact. We've linked directly to the official government sources so you can verify the details and apply correctly.BC First Time Home Buyers' Program — Property Transfer Tax ExemptionWhen you purchase a home in BC, you pay Property Transfer Tax at 1% on the first $200,000, 2% on the portion up to $3,000,000, and 3% above that. On an $800,000 purchase that's $14,000 in PTT. As a first time buyer you may be exempt from this entirely, or partially exempt, depending on the purchase price.Full exemption applies to purchases up to $835,000 as of 2024. Partial exemption applies between $835,000 and $860,000. Above $860,000 the exemption does not apply.Official details and eligibility requirements: https://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax/exemptions/first-time-home-buyersBC Home Buyer Rescission PeriodBC introduced a three business day rescission period for residential property purchases. This gives buyers the right to rescind an accepted offer within three business days, subject to a fee of 0.25% of the purchase price. This is a meaningful consumer protection that applies to most residential transactions.Official details: https://www2.gov.bc.ca/gov/content/housing-tenancy/home-ownership/buying-a-home/home-buyer-rescission-periodFederal First Home Savings Account (FHSA)The First Home Savings Account is one of the most powerful tools available to first time buyers in Canada right now. You can contribute up to $8,000 per year to a maximum of $40,000 lifetime. Contributions are tax deductible like an RRSP, and withdrawals for a qualifying home purchase are tax-free like a TFSA. If you have not opened one yet, open one immediately regardless of how far away your purchase is — contribution room does not accumulate until the account is open.Official details: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.htmlFederal Home Buyers' Plan — RRSP WithdrawalThe Home Buyers' Plan allows first time buyers to withdraw up to $35,000 from their RRSP tax-free to use toward the purchase of a qualifying home. If you are purchasing with a partner who is also a first time buyer, you can each withdraw up to $35,000 for a combined total of $70,000. The withdrawal must be repaid to your RRSP over 15 years.Official details: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan.htmlFederal First Time Home Buyer IncentiveThe federal government has offered a shared equity program for first time buyers. Check the current status and eligibility of this program directly as the details have been updated since its original launch.Official details: https://www.placetocallhome.ca/fthbi/first-time-homebuyer-incentiveGST New Housing RebateIf you are purchasing a newly built home or a substantially renovated property, you may be eligible for a partial GST rebate. This is particularly relevant for first time buyers considering presale or new construction on the North Shore.Official details: https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4028/gst-hst-new-housing-rebate.htmlWhat Does a First Time Buyer's Budget Actually Look Like in North Vancouver?

North Vancouver is not an inexpensive market. Being realistic about what your budget gets you is the starting point for a smart search.As a general guide for 2026:Condos in North Vancouver are the most accessible entry point for first time buyers, with a range of options across Lower Lonsdale, Central Lonsdale, and Lynn Valley starting in the mid to upper $500,000s for a one bedroom and approaching $800,000 and above for a well-located two bedroom in a newer building.Townhomes represent the next step up, with entry points typically in the $900,000 to $1,200,000 range depending on size, location, and condition.Detached homes are generally beyond the reach of a first purchase for most buyers without significant family support or unusually strong income and savings. That's not a discouraging statement — it's an accurate one. Starting with a well-chosen condo or townhome and building equity is how most North Shore homeowners eventually get to a detached home.Your mortgage broker will give you the exact numbers based on your income, down payment, and debt situation. The point here is to go into the search with realistic expectations rather than discovering the gap between expectation and reality at an open house.Where First Time Buyers Are Purchasing on the North Shore

First time buyers in North Vancouver are spread across the market, but a few areas consistently offer the most accessible entry points:Lower Lonsdale is the most active condo market on the North Shore. Strong transit connection via SeaBus, walkable neighbourhood, range of building ages and price points. A practical and livable first purchase for buyers who want urban convenience.Central Lonsdale offers a mix of older and newer condo inventory at generally more accessible prices than Lower Lonsdale. Good value, established neighbourhood, strong transit access.Lynn Valley has a strong townhome market and some condo inventory. Popular with first time buyers who want more space and a family-oriented neighbourhood character. Slightly more driving-dependent than Lonsdale.Lynnmour is a neighbourhood worth knowing. Townhome inventory at price points that work for first time buyers, good access to Lynn Valley and the highway, and a community that is evolving positively.Beyond North Vancouver — the Tri-Cities and beyond. Not every first time buyer's first purchase is in North Vancouver. Coquitlam, Port Moody, and Port Coquitlam offer significantly more purchasing power at equivalent budget levels and remain practical options for buyers with flexibility on location. We work across Greater Vancouver and can help you evaluate whether the right first purchase is on the North Shore or in a neighbouring area that gives you more for your money.The Buying Process — Step by Step

Step 1: Understand your finances. Know your down payment, your income, your debts, and your full budget including closing costs before anything else.Step 2: Get pre-approved. Work with a mortgage broker or your bank to get a formal pre-approval. This takes one to three days and is the single most important thing you can do before you start looking.Step 3: Define your priorities. Neighbourhood, property type, must-haves, and deal-breakers. The clearer you are before you start, the better decisions you make under pressure.Step 4: Start your search with an agent. An experienced local agent gives you access to listings as they come to market, knowledge of which buildings and complexes are worth considering, and guidance on pricing so you know what a fair offer looks like.Step 5: Make an offer. When you find the right property, your agent will prepare a written offer including your price, completion date, and any subjects such as financing and inspection. In competitive situations your agent will advise on offer strategy.Step 6: Complete your due diligence. Once an offer is accepted, you have a defined period to complete your subjects. This typically includes a home inspection and confirming your financing with your lender.Step 7: Remove subjects and complete. Once satisfied with your due diligence, you remove your subjects and the deal is firm. Your lawyer or notary handles the legal and financial aspects of closing.Step 8: Take possession. On completion day the funds transfer, title is registered in your name, and you get the keys.What to Expect From the Market as a First Time Buyer in 2026

North Vancouver is currently in buyer's market territory on detached homes, with more balanced conditions on condos and townhomes. For first time buyers this is a more forgiving environment than 2021 and 2022 — you generally have time to conduct proper due diligence, the pressure to waive conditions is lower, and days on market have stretched.That said, well-priced properties in desirable buildings and locations still attract competition. Being pre-approved, knowing the market, and having a clear strategy before you start looking remains essential.Talk to the Wallace Green Team

Buying your first home is a process that benefits enormously from having the right people around you. We work with first time buyers across the North Shore and Greater Vancouver and enjoy the process of helping people make a well-informed, well-prepared first purchase.If you're thinking about buying your first home and want a direct, honest conversation about what your budget gets you, where to look, and what the process looks like, Scott, Carson, and Jamie are easy to reach.