Steps in the buying process

Financial Pre-Approval: Clear understanding of what you can afford. Contacting a mortgage broker who will determine what you can afford based on income and down payment. If you don’t have a mortgage broker we can have one contact you.

- Driver's License or government issued photo ID

- Details of your employment (time at job, title, and income structure)

- Your sources of income

- Asset list

A mortgage pre-approval with a Mortgage Broker has many advantages, some of these are:

- Rate holds, A rate hold is generally 90 - 120 days and can protect you from rate hikes during that time.

- Determining a maximum purchase price to help streamline the home buying process

- The Ability to come up with a monthly budget

- Finding out your credit score and potentially working with your broker to help improve credit if needed

- Being prepared come time to write an offer (knowing which documentation is needed in advance)

- The ability to close a mortgage loan faster

- Mortgage rules and rates are always changing, having a mortgage professional on your side to look out for your best interest and keep you in the loop.

Agency: When we represent you as a buyer we are working within a legal relationship called an ‘agency’. The agency exists between you, the client, and the company under which we are licensed. We provide you with a ‘working with a real estate agent’ document to disclose the nature of the relationship.

Dual Agency: Dual agency occurs when an agent represents both the buyer and the seller in a single transaction. A dual agent must be impartial to both the buyer and the seller and fully disclose all the information relating to the transaction. Bother the seller and the buyer must agree in writing to dual agency.

The Search: This is where things get fun and we begin to start vigorously searching for your perfect home. We are thoroughly searching every day for homes that fit your criteria. We carefully monitor what in on the market, what is new to the market and what is coming to the market. You will be updated regularly and we can arrange to view homes at your convenience.

The Offer

When you find a home you are interested in purchasing, your Real Estate Agent will write up a Purchase and Sale Agreement. This document typically contains:- Property address

- Purchase price + Deposit amount

- Subjects and subject removal date, closing date and possession date

- All items included in the sale

- Any conditions & terms to protect you as the buyer

- Subject to financing

- Subject to inspection

- Subject to receiving and approving the minutes, property disclosure statement, bylaws, financials etc...

- Subject to appraisal

The following should be done between subject removal and possession date if applicable:

- Give notice to your landlord / strata

- Hire a mover or reserve a truck if you plan on doing it yourself (book elevators)

- Register a mail change

- Arrange for property insurance

- Talk to your Financial Advisor about Life and Disability Insurance

- Your Lawyer/Notary should receive the entire mortgage and purchase paperwork from your Realtor and Mortgage Broker. The Lawyer/Notary will contact you to make an appointment with you usually three to four days before closing. At this meeting you will need to bring a bank draft to cover the remaining closing costs (they will let you know the exact amount for this prior to the appointment), proof of insurance and photo ID

- Receive the money from your mortgage lender

- Pay the seller

- Register the mortgage and the title at the Land Titles Office

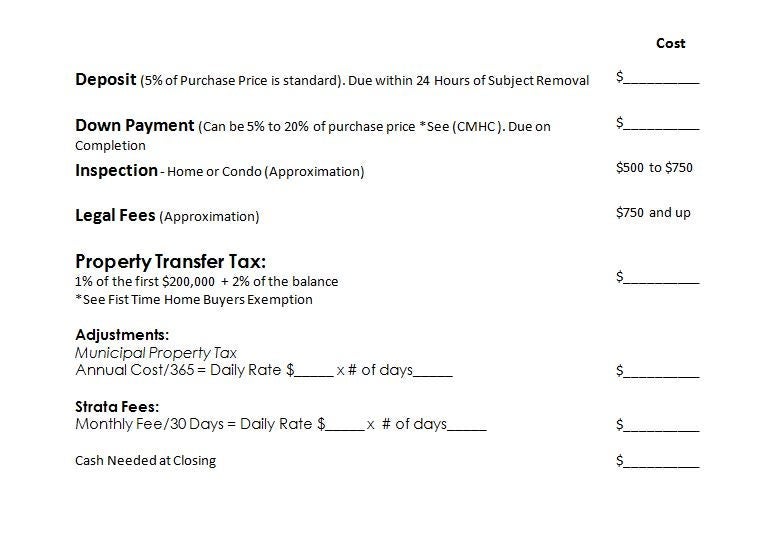

Closing Costs Worksheet

*CMHC

Mortgage loan insurance is typically required by lenders when homebuyers make a down payment of less than 20%. See additional pages on CMHC

*First Time Home Buyers Tax Exemption

If you purchase your first home under $425,000 you may be eligible for a property transfer tax exemption. There is also a sliding scale between $475,000 and $500,000 that you may receive partial rebates

Helpful Terms

Contract of Purchase and Sale: This document includes every condition in your offer to purchase your condo or home. Price, dates, conditions, and everything else is included in this document.Deposit: is held by the buyer’s REALTOR’s company in a trust until completion and put towards the price. Closer to 5% the more serious the offer will be taken. Failure to pay deposit on time results in breach of contract. Usually 24 to 48 hours after final subject removal. Must be bank draft and is payable to TAC Real Estate Corp in Trust.

Completion: Is the day that the money for the purchase is paid to the Seller by the Buyer. This is typically one to two days before the Possession Day.

Possession: Is the date the Buyer has the right to take possession of the property.

Adjustments: Is the date that the calculations for items such as property taxes, water accounts, rents, damage deposits, etc. are modified. These charges are adjusted by your lawyer.

Included Items: Are fixtures (anything secured to the property) that stay unless excluded by the seller. Chattels (anything not fixed to the property) must be written in the offer. Typically we would ask for all appliances and window coverings.

Title (Freehold or Leasehold): Legal possession. A freehold title gives the holder ownership of land and buildings for an indefinite period of time. A leasehold title gives the holder a right to use and occupy land and buildings for a defined period of time. In a leasehold arrangement, actual ownership of the land, sometimes along with the buildings, remains with the landlord.

Appraisal: An estimated value of a property that is completed by a certified appraiser for mortgage financing.

Closing Costs: Costs, in addition to the purchase price of your home, such as legal fees, transfer fees and disbursements, that are payable on the closing date. Closing costs typically range from 2%-4% of the purchase price.

Pre-Approved Mortgage: When a lender approves the potential mortgage for a specific amount, based on how much money the lender is prepared to lend the borrower. This allows buyers to shop for homes that they already know they can afford.